Worried about securing a steady income after retirement? Or looking for a low-risk way to generate passive earnings? In today’s fast-paced world, having a stable financial plan is more important than ever.

The Monthly Income Scheme (MIS) is a low-risk investment plan that provides guaranteed returns with capital protection and scheduled payments. The financial security provided by Monthly Income Schemes (MIS) benefits all types of individuals including retirees and homemakers as well as those who want to secure their financial future.

In this guide, we’ll explore the best monthly income schemes in India, their benefits, and how you can maximize your returns!

Section

Details

What is MIS?

A low-risk investment option providing regular fixed income, ideal for retirees and homemakers.

Key Features

– Guaranteed returns – Fixed tenure (5–10 years) – Competitive interest rates – Easy access for all

Top MIS Options

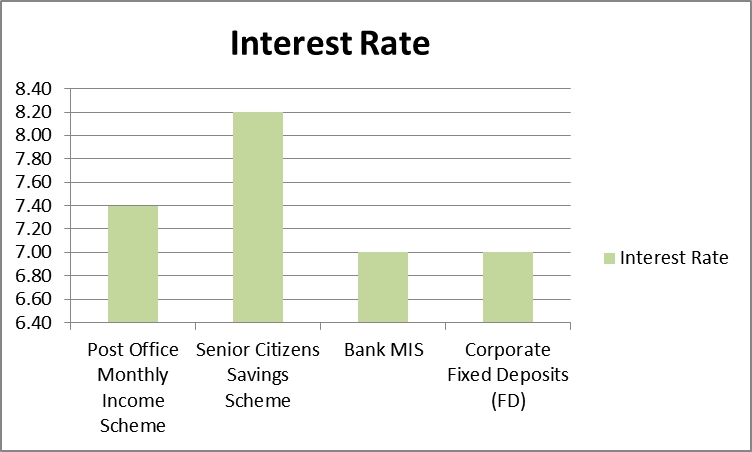

– POMIS: 7.4% interest, ₹1,000–₹9 lakh, 5-year tenure – SCSS: 8.2% interest, up to ₹15 lakh, 5 years + 3 years – Bank MIS: 4-7% interest, flexible tenure – Corporate FDs: 7–9% interest, higher risk

If you go for a Monthly Income Scheme (MIS), it is a low-risk investment option, which provides investors with regular fixed income. The basic idea behind MIS is to offer interest payouts at regular intervals that vary from 6 months to 3 years are given typically by banks, financial institutions and post offices. They are especially popular with retirees and individuals wishing to build a stable income.

Key Features of Monthly Income Schemes

Guaranteed Returns: For risk-averse investors, MIS ensures predictable monthly payouts, making it a smart choice for stable, low-risk investments. The returns are fixed unlike market linked investments and as a result are not dependent on market volatility.

Fixed Tenure: MIS typically has a fixed tenure of 5 to 10 years. Upon maturity, investors can either withdraw their principal or reinvest in another scheme.

Capital Safety: These schemes are intended to defend the first capital investment and assure you that the money you work so hard for is safe.

Attractive Interest Rates: The interest rates for Monthly Income Schemes vary based on the provider, but they are generally higher than regular savings accounts, making them one of the best investment plans for senior citizens and homemakers.

Accessibility: MIS is provided to a lot of different investors like senior citizens, professionals on salary, homemakers etc. Just as there are many providers, there are also many joint account options for your added convenience.

Top Monthly Income Schemes in India

1. Post Office Monthly Income Scheme (POMIS)

The Post Office Monthly Income Scheme (POMIS) is one of the safest and most popular options for generating a steady monthly income. Backed by the Government of India, it offers:

Interest Rate: Approximately 7.4% annually (subject to revision).

Investment Limit: Minimum ₹1,000/- and maximum ₹9 lakh for joint accounts.

Tenure: 5 years.

Tax Benefits: Tax on interest is payable and not TDS.

2. Senior Citizens Savings Scheme (SCSS)

Designed for individuals aged 60 and above, the SCSS offers higher returns than standard MIS options, making it an attractive choice for retirees. Features include:

Interest Rate: Around 8.2% annually.

Maximum Investment: ₹15 lakh.

Tenure: 5 years (can extendable by 3 years).

Tax Benefits: Hence it qualifies for being tax deducted under Section 80C.

3. Monthly Income Plans by Banks

MIS is also available as Bank Monthly Income Schemes variant with the same banks, where the monthly interest is available. The specifics vary, but typically:

Interest Rate: Between 4% to 7%.

Tenure: Flexible, ranging from 1 to 10 years.

Minimum Investment: Varies by bank.

4. Corporate Fixed Deposits

With slightly higher risks corporate fixed deposits are available to investors willing to take the risk. However, they lack government backing.

Interest Rate: 7% to 9%.

Tenure: 1 to 5 years.

Risks: A lack of insurance coverage, credit risk.

Advantages of Monthly Income Schemes

Regular Income: MIS ensures a steady cash flow, making it ideal for retirees and individuals who rely on fixed income for daily expenses.

Risk Mitigation: MIS options are mostly low risk ways to protect your capital from market swings.

Diversification: Including MIS in your portfolio helps balance high-risk and low-risk investments, enhancing financial security.

Flexibility: The scheme will enable investors with the liberty to select the tenure they wish to invest in and also interest payout scheme that suits their financial goals.

Tax Benefits: Some of these schemes like SCSS are provided tax deductions as per certain provisions of the Income Tax Act.

Pre-Requisites to Consider When Selecting a Monthly Income Scheme

Interest Rates: To choose the provider with the best interest rates, you can compare those interest rates across varying providers.

Lock-in Period: Take your tenure to evaluate how the scheme can hold your financial needs.

Tax Implications: Know how interest income is taxable and whether scheme is eligible for the deduction.

Premature Withdrawal: In case of unforeseen circumstances you can check if there are penalties or restrictions on premature withdrawals.

Inflation Adjustments: Include inflation into your equation so that the real value of your returns doesn’t intact over time.

How to Open a Monthly Income Scheme Account: Online and Offline

Opening an MIS account is simple, with both online and offline options available. You can choose to open the account in either online or offline based on your own preference. Below is a step by step guide for your both methods.

Before applying for an MIS investment, ensure you meet the eligibility for monthly income schemes requirements:

Age Requirement: Most schemes require the applicant to be at least 18 years old. For schemes like the Senior Citizens Savings Scheme (SCSS), the oldest age as permitted for the scheme is 60 years.

Citizenship: Generally, these schemes are available to Indian residents. NRIs would have to be examined under some schemes.

2. Required Documentation

The following documents are mandatory for opening an MIS account:

Proof of Identity: Photo identity card – Aadhaar card, Permanent Account Number (PAN) Card, Indian Passport or Driving License.

Proof of Address: Aadhaar card, voter ID, rental agreement or such utility bill.

Photographs: Passport-sized photographs.

Bank Account Details: A canceled cheque or passbook copy to link your account for monthly payouts.

KYC Compliance: This means you need to go through complete Know Your Customer (KYC) formalities as required by the provider.

How to Open an MIS Account Offline

Alternatively, if you would like to do things the old fashioned way, you can go to the local branch of your preferred provider. Follow these steps:

Step 1: Visit the Branch

Visit the post office, bank or financial institution offering the MIS.

Collect the application form from the branch.

Step 2: Fill Out the Form

Provide correct detail with personal details, nominee details, and account preferences in the form.

Attach the required documents and same photograph sized passports.

Step 3: Submit the Application

Complete the form and submit it along with the initial deposit (via cash, cheque, or demand draft) at the branch.

They will take and process your application and verify the documents.

Step 4: Receive Confirmation

If the verification is successful, you will get a passbook or an acknowledgment slip of your MIS account.

Tips to Help You Get the Most From Monthly Income Schemes

Reinvest Monthly Payouts: Instead, you use the monthly income to invest into other low-risk investment plans for compounded growth.

Opt for Joint Accounts: One can increase investment limit by opening joint account.

Diversify Across Providers:Divide your investments in different ways to reduce risks and maximize returns.

Leverage Tax Benefits: Choose tax-saving investment schemes like SCSS to reduce taxable income.

FAQs on Post Office Monthly Income Scheme

1. What is a Monthly Income Scheme (MIS)?

A Monthly Income Scheme (MIS) is a low-risk investment plan that provides fixed monthly payouts to investors. Retirees along with homemakers and passive income seekers find this option suitable for their needs.

2. Which Monthly Income Scheme offers the highest returns?

As of 2024, the Senior Citizens Savings Scheme (SCSS) offers the highest return at 8.2% interest, followed by Corporate FDs (7-9%) and Post Office MIS (7.4%).

3. Is Monthly Income Scheme taxable?

Yes, the interest earned from MIS is taxable as per your income tax slab. However, SCSS qualifies for tax deductions under Section 80C.

4. Who is eligible for a Monthly Income Scheme?

Eligibility varies by scheme: POMIS: Indian residents, 18+ years SCSS: Only for senior citizens (60+ years) Bank MIS & Corporate FDs: Available for most Indian residents

5. Can I withdraw my investment before maturity?

Yes, but premature withdrawal penalties apply. For example, in POMIS, withdrawals before 1 year are not allowed, and between 1-3 years, a penalty applies.

6. How do I open a Monthly Income Scheme account?

You can open an MIS account both online and offline: The process of opening a bank account requires visiting either a bank or post office while presenting KYC documents. The digital option allows users to apply through internet banking or mobile apps.

7. What is the minimum and maximum investment limit for MIS?

Post Office MIS: ₹1,000 (min) – ₹9 lakh (max for joint accounts). SCSS: Up to ₹15 lakh. Corporate FDs & Bank MIS: Limits vary by provider.

Yes, Government-backed schemes POMIS and SCSS offer complete safety to investors. Bank MIS and Corporate FDs have slightly higher risks, but they also offer higher returns.

9. How can I maximize returns from a Monthly Income Scheme?

To increase your returns, you can: Reinvest monthly payouts into another investment plan. Opt for joint accounts to increase investment limits. Divide the investments across different MIS providers to balance risk and reward.

10. Which is better: Fixed Deposit (FD) or Monthly Income Scheme (MIS)?

MIS delivers consistent monthly payments which makes it suitable for generating passive income. The compounding nature of Fixed Deposits results in increased long-term growth through time. If you need monthly income, choose MIS; if you can wait for maturity, go for FDs.

Final Thoughts on Monthly Income Scheme

A Monthly Income Scheme (MIS) is an excellent way to secure financial stability while generating passive income. MIS serves as a dependable solution for managing retirement planning and household finances as well as low-risk investments.

Your ability to select the right MIS option depends on your knowledge of their features alongside their benefits and eligibility requirements. Don’t wait—start investing in an MIS today and enjoy the peace of mind that comes with a steady, guaranteed monthly income!

Skip to content

Skip to content