Imagine a future where your daughter’s education, career, and dreams are fully funded, regardless of the financial challenges life throws her way. Sounds like a distant dream? Not anymore.

The Sukanya Samriddhi Yojana (SSY) is here to turn that dream into reality. The government-sponsored savings program provides substantial returns together with tax benefits and financial protection to empower women and their families. Whether you’re planning for her education or her big wedding day, SSY is your key to ensuring that her future is as bright as her potential.

Keep reading to learn how you can start creating a strong financial foundation for your daughter’s success now.

Feature

Details

Interest Rate

8.2% per annum

Tenure

21 years (or upon marriage after 18 years)

Minimum Contribution

₹250 per year

Maximum Contribution

₹1.5 lakh per year

Premature Withdrawal

Allowed after 18 years (for education, up to 50% of balance)

Tax Benefits

Under Section 80C (up to ₹1.5 lakh), Tax-free interest and maturity

Lock-in Period

21 years

Eligibility

For girls under 10 years (only one account per girl)

Account Holder

Parents/Guardians of a girl child

Maturity Period

21 years from account opening or upon marriage after 18

Transferability

Yes, can be transferred between banks/post offices

Risks

Government-backed, very low risk

What is Sukanya Samriddhi Yojana?

Overview: The main objective of SSY is to develop positive attitudes towards the girl child. Through this account, savings promote savings. It opens up a world of no discrimination within the money limitations.

Essence of financial Planning:SSY is for those families that have built their career on the bright future of their daughters. The long-term financial goal of higher studies or marriage can be achieved by availing disciplined savings over tenure.

SSYaccounts can either be opened by biological parents or the legal guardians of girl children who are aged less than 10 years. Each family may open a maximum of two accounts for two daughters.

The lock-in period: The maturity period is for 21 years from the date of commencement of the account or upon marriage of the account holder after she turns 18. That is to avoid any premature withdrawal.

Interest Rate: One of the highest interest rates among government-supported savings schemes, the interest paid on Sukanya Samriddhi is quarterly, ensuring that the plan stays grounded in reality amid inflation.

Benefits of Sukanya Samriddhi Yojana

Tax Benefits: There is liability to tax for donation to SSY made under Section 80C of the Income Tax Act. The interest that accrues or the maturity amount can be completely exempt from tax such as PPF.

Higher Interest Returns: SSY‘s provide higher rates of interest than savings accounts and fixed deposits so that savers want to build up an enormous nest egg over time.

Financial Security for Daughters: A SSY offers that sort of security that ensures the parent that the cost of education and marriage-or any other big milestone that comes up in the life of that girl-need not cause them financial distress.

Financial Security for Daughters: A SSY offers that sort of security that ensures the parent that the cost of education and marriage or any other big milestone that comes up in the life of that girl-need not cause them financial distress.

Process to Open an Account

Documents Required

For operating an SSY account:

A birth certificate of the girl child.

Proof of identity; that is, Aadhaar or PAN.

Proof of residence (like electric or water supply bill or Aadhaar number).

Procedure for Opening

Approach any bank or post office where the scheme is available.

Fill in the SSY application form.

Submit the appropriate documents.

Make the first installment (minimum ₹250).

The account opening may be confirmed through using the post or bank passbook issued by the bank.

Criteria for Eligibility Explained

Who Can Open?

Girl Child’s parent or legal guardian alone can open account under Sukanya Samriddhi Yojana. Secondly, at the point this account was opened the girl child should be less than 10 years. Additionally, families may open two accounts for two girls from the same family.

Age Limitations

The account needs to be opened before the girl child turns 10 years old. Thereafter, any contributions can continue to be made until the child reaches an age of 15 years, alongside which the account matures 21 years from the date of its opening.

The minimum contribution per financial year is ₹250, while the maximum contribution may not exceed ₹1.5 lakh. Since SSY permits a wide range of contributions, this implies that families from any economic stratum may make contributions.

Annual Deposit Rules

Contributions may be made in a single or lump sum or throughout the year in installments. If a deposit is missed, a penalty of ₹50 is charged, to be paid together with the relevant yearly payment to reactivate the account.

Behavior of Interest Rates

Current Trends: Current SSY interest is pegged at 8.2% per year and compounded annually. The government changes it frequently.

How Interest Rates Work: Interest is calculated on the lowest daily balance in the account during the period between the close of the fifth and the last day of each month. This strategy will assure that account holders get fair and clear returns.

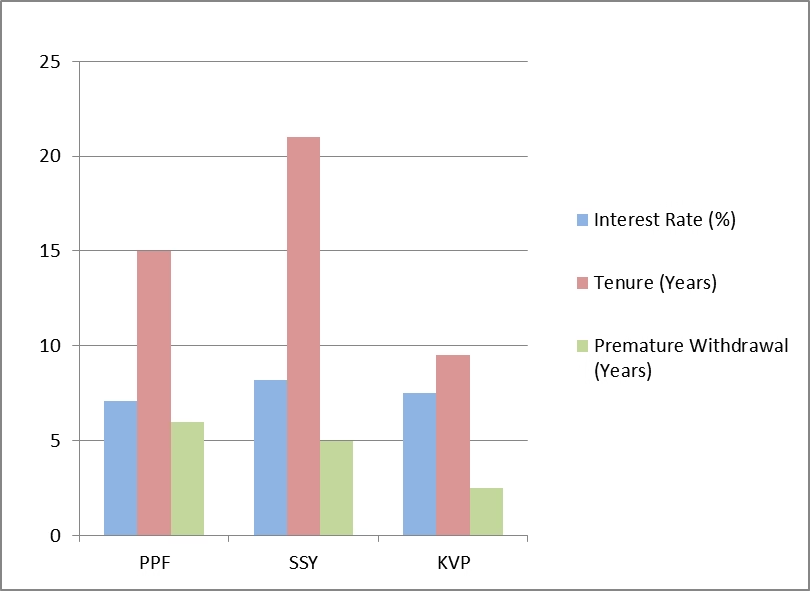

Feature

PPF

SSY

KVP

Interest Rate (%)

7.1

8.2

7.5

Tenure (Years)

15

21

9.5

Premature Withdrawal (Years)

6

5

2.5

Comparing interest rates, tenure, and premature withdrawal options of PPF, SSY, and KVP in a detailed bar graph.

Exemptions and Allowances

Section 80C Benefits: Sukanya Samriddhi Yojana permits tax benefits for investment under Section 80C of the Income Tax Act of a maximum of ₹1.5 lakh in a financial year.

Tax-Free Interest: For SSY the fund gives all the maturity amount and SSY rate of interest as complete tax exemption. It falls under the EEE (Exempt-Exempt-Exempt) category which means contributions are tax free, it also qualifies for tax free growth and tax-free withdrawals; a great choice for mothers and guardians to make for financial security.

Frequently Asked Questions (FAQs)

1.What happens if I miss a deposit?

Missing a deposit incurs a penalty of ₹50. The account can be reactivated by paying the penalty along with the minimum annual contribution.

2.Can I transfer my account?

Yes, SSY accounts can be transferred between banks and post offices, or between branches, without any charges.

3.Is partial withdrawal allowed?

Partial withdrawal of up to 50% of the balance is permitted after the girl child turns 18, for educational purposes.

The account matures 21 years from the date of opening or upon the marriage of the account holder after the age of 18.

5.Can I open multiple accounts for one child?

No, only one account per girl child is allowed under the SSY scheme.

6.Are there any risks involved?

As a government-backed scheme, SSY is a safe avenue for investment guaranteeing returns with little scope for risk.

7. How can I open an SSY account?

Have your bank or post office provide you with the application form, fill and submit the documents along with the first deposit of min ₹250.

8. Can I make a one-time deposit or yearly installment?

Both options are allowed. You can contribute in one lump sum or yearly installments.

9. What is the penalty for missing a contribution?

For missing contributions, a penalty of ₹50 is levied. To re-activate the account, the penalty and the number of missed contributions must be paid.

10. Can I use SSY for my daughter’s marriage or education?

Yes, partially withdrawn in SSY can be made only on educational purpose when the child turns 18 in age.

Success Stories

Success Story 1: Meera’s Medical Dream

Meera’s parents in Pune opened an SSY account in 2010 to fund her dream of becoming a doctor. Thanks to the high interest rates and tax benefits, the account grew steadily. By the time she completed school, the money was sufficient to pay her medical education, allowing her to concentrate on her studies without financial constraints.

Today, Meera is a proud doctor, all thanks to SSY.

Success Story 2: Priya’s Wedding Fund

Priya’s family from Tamil Nadu opened an SSY account in 2012 to secure her future. By the time Priya turned 18, the account had grown sufficiently to fund her wedding expenses. With no need for loans, her parents were able to give her the wedding of her dreams.

Today, Priya is thriving in her career, and her parents are grateful for the financial security SSY provided.

Success Story 3: Shalini’s Business Start-Up

Shalini’s parents in Bangalore started an SSY account for her in 2015. By the time she graduated, the account balance helped fund her entrepreneurial dream starting her own boutique. The financial cushion from SSY allowed Shalini to take the leap and turn her passion into a successful business.

Challenges and Limitations

Lock-in Period Concerns: Somewhat ironically, this extended lock-in period may turn off some investors. Yet it guarantees that funds remain available for key mile stones.

Inflation Adjustments: Interest rates in SSY often cannot keep up with inflation though it has unusually high returns. This decision is reviewed periodically by the government.

Maximizing Benefits Expert Tips

Strategic Deposits: When contributing the maximum amount, they should do so at the beginning of the financial year so the greatest interest earnings are made.

Interest Rate Updates: You should keep track of quarterly interest rate updates so that you can plan you contributions effectively.

Sukanya Samriddhi Yojna: How This Scheme Is Helping Women

Promoting Education: SSY makes financial constraints a barrier to a girl’s education, promoting equality and empowered.

Achieving Financial Independence: They make sure that you become financially free. Secondly, SSY will encourage savings among daughters which will be used for the daughters to become economically liberated and secure.

Proposed changes: The government bid to improve the SSY scheme into an entirely alluring proposition with higher contribution limits accompanied by additional tax benefits.

Projected growth: There is much buzz about the rise of SSY, owing to an extensive outreach for enabling savings for the future of millions of families with girls among their children.

Sukanya Samriddhi Yojana isn’t simply a savings program it’s a strong, government-backed weapon that promises a secure future for your daughter. The tax benefits together with high interest rates and mandatory lock-in period establish SSY as an optimal financial tool for families intending to safeguard and assist their daughter’s future ambitions.

Now is the time to take charge of her future. Don’t let financial worries limit her potential. Open an SSY account today, and start building a foundation that will last a lifetime.

Your daughter’s brighter future starts with you, secure it now!

Skip to content

Skip to content