Want to grow your savings effortlessly while keeping your investment 100% safe? With the Post Office Recurring Deposit (RD), you get a 6.7% interest rate in 2025, quarterly compounding, and government-backed security, ensuring steady, risk-free growth for your money.

Perfect for salaried employees & risk-averse investors, this scheme guarantees stable returns while giving you the flexibility to start with as little as ₹100 per month!

Turn small savings into big returns, invest in a Post Office RD now! In this guide, we’ll cover everything you need to know: the latest interest rates, benefits, eligibility, and how to maximize your returns.

Post Office RD Interest Rate – Overview

Category

Details

Scheme Name

Post Office Recurring Deposit (RD)

Managing Authority

India Post, under the Ministry of Communications

Current Interest Rate (2024)

6.7% per annum (compounded quarterly)

Tenure

5 years (extendable in 5-year blocks)

Minimum Deposit

₹100/- per month

Compounding Frequency

Quarterly

Government Backing

Yes (Risk-free investment)

Loan Facility

Up to 50% of the deposit amount after 12 months

Premature Withdrawal

Allowed after 3 years (with penalty)

Eligibility

Indian Residents, Minors (above 10 years), Joint Accounts (2 adults)

Opening Methods

Offline (Post Office) & Online (India Post Payments Bank – IPPB)

Taxation

No TDS, but interest is taxable under “Income from Other Sources”

Interest Calculation Formula

Compound Interest Formula

Example Calculation

₹5,000/- month for 5 years at 6.7% results in ₹3,49,819 at maturity

Comparison with Bank RD

Competitive interest rates, government guarantee, lower minimum deposit

Key Benefits

Guaranteed returns, high liquidity, tax benefits, loan availability

Latest Post Office RD Interest Rates (2024)

The current interest rate of Post Office RD is 6.7% per annum allows users to receive quarterly compound interest over 5 years. Every quarter Post Office RD adjusts its interest rate according to both prevailing economic conditions and government policy updates.

Tenure

Interest Rate (Per Annum)

5 Years

6.7% (Compounded Quarterly)

Quarterly compounding boosts your overall returns, helping your savings grow even more.

Key Features of Post Office RD Scheme

Guaranteed Returns: The Post Office RD provides users with stable interest rates which creates a secure investment choice.

Low Minimum Deposit: Anyone can start investing with just ₹100 per month, making it accessible to all.

Government-Backed Scheme: Since the Indian government backs this scheme, your investment is 100% risk-free.

Compounded Quarterly: Investments experience compound interest growth every 3 months to deliver improved earnings.

Flexible Investment Tenure: The default investment period lasts 5 years although additional five-year blocks allow investors to extend their commitment.

Loan Facility: After 12 months of deposit investors can access up to 50% of their money as a loan.

Premature Withdrawal: Allowed after 3 years, subject to a penalty.

How to Calculate Interest on Post Office RD?

The interest on a Post Office RD is calculated using the compound interest formula.

An investment at 6.7% annual interest grows ₹5,000/- monthly Just five years contributions lead to ₹3,49,819/-. Know more about PPF, SCSS, NSC & KVP etc.

Eligibility Criteria for Post Office RD

To open a Post Office RD account, the following eligibility criteria must be met:

Indian Resident: Only citizens who hold Indian nationality are permitted to create an account.

Minor Accounts: Children over 10 years of age can create individual bank accounts.

Joint Accounts: Joint accounts can be opened by two adult individuals jointly.

How to Open a Post Office RD Account?

Opening a Post Office RD account is simple and can be done through both offline and online methods:

Offline Method:

Visit the nearest Post Office.

Collect and fill the RD Account Opening Form.

Submit the following KYC documents for identity verification: Verification completion triggers a requirement for Aadhaar in combination with a PAN card and a recent photograph dated within three months.

Make the first installment payment either in cash or by cheque.

Once your account is processed, you’ll receive your RD passbook.

Online Method (For India Post Payments Bank Users):

To access your India Post Payments Bank (IPPB) account view sign in.

Navigate to the RD account opening section.

Enter all the necessary personal information they ask for and decide on the amount you want to deposit each month into your RD account.

Finish the transaction, and you will get a confirmation message for your new RD account.

Benefits of Investing in Post Office RD

Risk-Free Investment: Since this scheme is supported by the government, there is absolutely no chance of losing your capital.

High Liquidity: Even though it has a set duration of 5 years, you can make partial withdrawals after 3 years.

Ideal for Small Investors: Requiring just a minimum deposit of ₹100/- each month, it’s perfect for those who save small amounts.

Loan Against RD: Up to 50% of the deposited amount can take as loan by investors after one year.

No TDS on Interest Earned: Unlike fixed deposits, there is no TDS deduction on Post Office RD interest, but the interest earned is taxable as per your income slab.

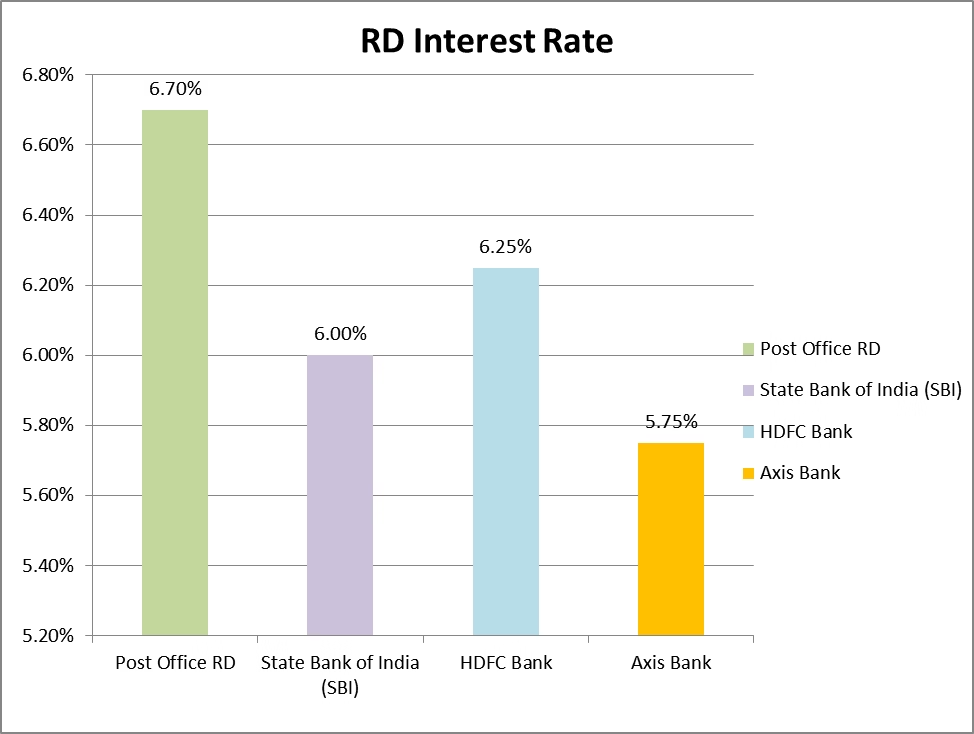

Post Office RD vs Other Bank RD – Which is Better?

Comparison of Post Office RD interest rates with SBI, HDFC, and Axis Bank in 2024, helping investors choose the best savings option.

Taxation on Post Office RD

No Tax Benefits Under Section 80C Deposits made in a Post Office RD do not qualify for deductions under Section 80C of the Income Tax Act.

Unlike 5-year Post Office Time Deposit, which offers tax-saving benefits, RD does not provide any tax exemption.

RD Interest Calculation Example

Scenario: Ramesh, a salaried employee, wants to save for his child’s education. He decides to invest ₹5,000 per month in a Post Office RD for 5 years at an interest rate of 6.7% (compounded quarterly).

RD Maturity Calculation:

Monthly Deposit: ₹5,000

Tenure: 5 Years (60 months) Interest Rate: 6.7% (compounded

Interest Rate: 6.7% (compounded quarterly)

Using the RD formula:

After 5 years, Ramesh’s maturity amount will be ₹3,56,830.

So, his total investment is ₹3,00,000 (₹5,000 × 60 months), and the total interest earned is ₹56,830.

RD Taxation Example

Scenario: Priya, an IT professional, has an RD where she deposits ₹10,000 per month for 5 years.

Total Deposit: ₹6,00,000 (₹10,000 × 60 months)

Total Interest Earned: ₹1,13,660 (at 6.7%)

Total Maturity Amount: ₹7,13,660

Tax Calculation (Based on New Regime – No Tax up to ₹12 Lakh). If Priya’s total annual income (salary + interest) is below ₹12 lakh, she pays no tax on the RD interest. If her income exceeds ₹12 lakh, the interest earned (₹1,13,660) will be taxed under “Income from Other Sources” at her slab rate.

Since Post Office RD does not deduct TDS, she must declare and pay tax while filing her ITR.

Scenario: Amit, a small business owner, has been investing ₹8,000 per month in an RD for the past 2 years.

Total Investment: ₹1,92,000 (₹8,000 × 24 months)

Interest Earned: ₹13,800

Total RD Balance: ₹2,05,800

Loan Facility:

Amit needs ₹1 lakh urgently for his business expansion. He can take a loan of up to 50% of his RD balance, which is ₹1,02,900 (50% of ₹2,05,800). The loan interest rate is typically 2% higher than the RD rate (6.7% + 2% = 8.7%).

Instead of breaking his RD and losing interest benefits, he uses the loan feature and repays it later while continuing his savings.

FAQs on Post Office RD

1. What is a Recurring Deposit (RD)?

The Recurring Deposit (RD) features in the financial offerings from banks and post offices because it allows customers to make regular monthly contributions at a specified rate of interest for a predetermined duration. When your term concludes you will get both your invested principal and accrued interest.

2. What are the benefits of investing in a Recurring Deposit?

Guaranteed returns: The interest from RDs maintains clear and definite rate of return. Financial discipline: Scheduled contributions through months enable people to establish savings practices. Safe investment: Post office RDs obtain government supported insurance as they represent minimal risk investments. Loan against RD: A few banking institutions let customers access loans by pledging their recurring deposit account funds. Tax benefits: The interest income from an RD stays taxable until you invest in a five-year certified product that qualifies for Section 80C deductions.

3. How does Post Office RD compare to bank RDs in terms of interest rates?

Under Post Office RD programs both general public and senior citizens earn an interest rate of 6.70%. General customers of SBI and HDFC experience interest rates varying from 5.75% to 6.50% above base while senior citizen rates reach between 6.25% to 7.00% above base.

Owners who withdraw their savings funds before maturity must pay penalties that total 1/2 to 1 percent of gained interest.

5. Is there a minimum or maximum tenure for Recurring Deposits?

The time period for Recurring Deposit schemes runs between 6 months up to 10 years at either post office locations or banks. Post Office RD maintains a single permanent term duration of 5 years.

6. Can I change the monthly deposit amount in an RD?

After starting a recurring deposit the bank system will not let you modify the regular payment amount. The amount on bank recurring deposits remains unchangeable until certain specific requirements are met or until completing all required tenure periods.

7. What is the minimum deposit amount for an RD?

Investors need funds in amounts starting from ₹100/- to open Post Office recurring deposit accounts. The deposit threshold for bank savings ranges between ₹100/- and ₹500/- monthly at institutions including SBI, HDFC and Axis Bank.

8. How is the interest calculated on RDs?

A fixed rate determines interest calculation through monthly compounding while the funds disburse at the end of the regulatory period. The interest rate used to calculate earnings in RD accounts remains constant from the day customers open their accounts.

9. Can I open an RD jointly?

Both banking institutions and post offices support joint RD’s that permit several contributors to receive their account total together at maturity.

10. What happens if I miss a monthly payment for my RD?

A single payment delay will cause the RD to lose interest benefits and could suspend its operations for a period. After missing a payment some financial institutions allow customers to pay it back within a prescribed grace period.

11. What is the tax treatment of RD interest?

Both public and private sector banks tax the earnings from RD accounts. TDS (Tax Deducted at Source) payments occur when banks identify interest amounts exceeding ₹40,000/- in a year or ₹50,000/– for those who qualify as senior citizens. The interest you earn adds to your overall income before being taxed according to your chosen income tax bracket.

12. What is the maximum amount I can invest in a Recurring Deposit?

Both Post Office RD and bank RDs have no set maximum investment limit beyond standard income tax thresholds. The amount of interest earned increases in a direct correlation to the size of your regular monthly investment.

13. Can i take a loan against on RD?

Various banking institutions enable customers to receive loans for up to 90% of their regular deposit amount though they impose unique lending standards.

14. Is the Post Office RD scheme safer than bank RDs?

The Post Office RD achieves full risk-free status because it receives backing from the Government of India. Bank RDs maintain security but investors face risk from unsound bank conditions.

You can start an RD account online via your bank’s web portal or smartphone application. Additionally you can initiate the account process by completing paperwork at either your bank’s facility or during a visit to any post office.

Final Thoughts

The Post Office RD is not only a savings plan but a secure, smart way to grow your wealth. It has a 6.7% interest rate with quarterly compounding and with full government backing, it is risk free and delivers consistent returns. This scheme is useful for you if you are a salaried employee or a cautious investor, as it allows you to develop a disciplined savings habit with ease.

Don’t wait and begin your Post Office RD today, where your money will grow safely and steadily!

Skip to content

Skip to content