Want to grow your savings securely?Kisan Vikas Patra (KVP) is a government-backed savings scheme that offers risk-free, long-term returns on an accrual basis. With an annual interest rate of 7.5% (compounded yearly), your investment will double in just 9 years and 5 months. In this guide, we’ll break down KVP’s features, benefits, and eligibility—and show you exactly how to invest today for a financially secure future. Don’t wait—start multiplying your wealth now!

Overview of KVP

Feature

Details

Interest Rate

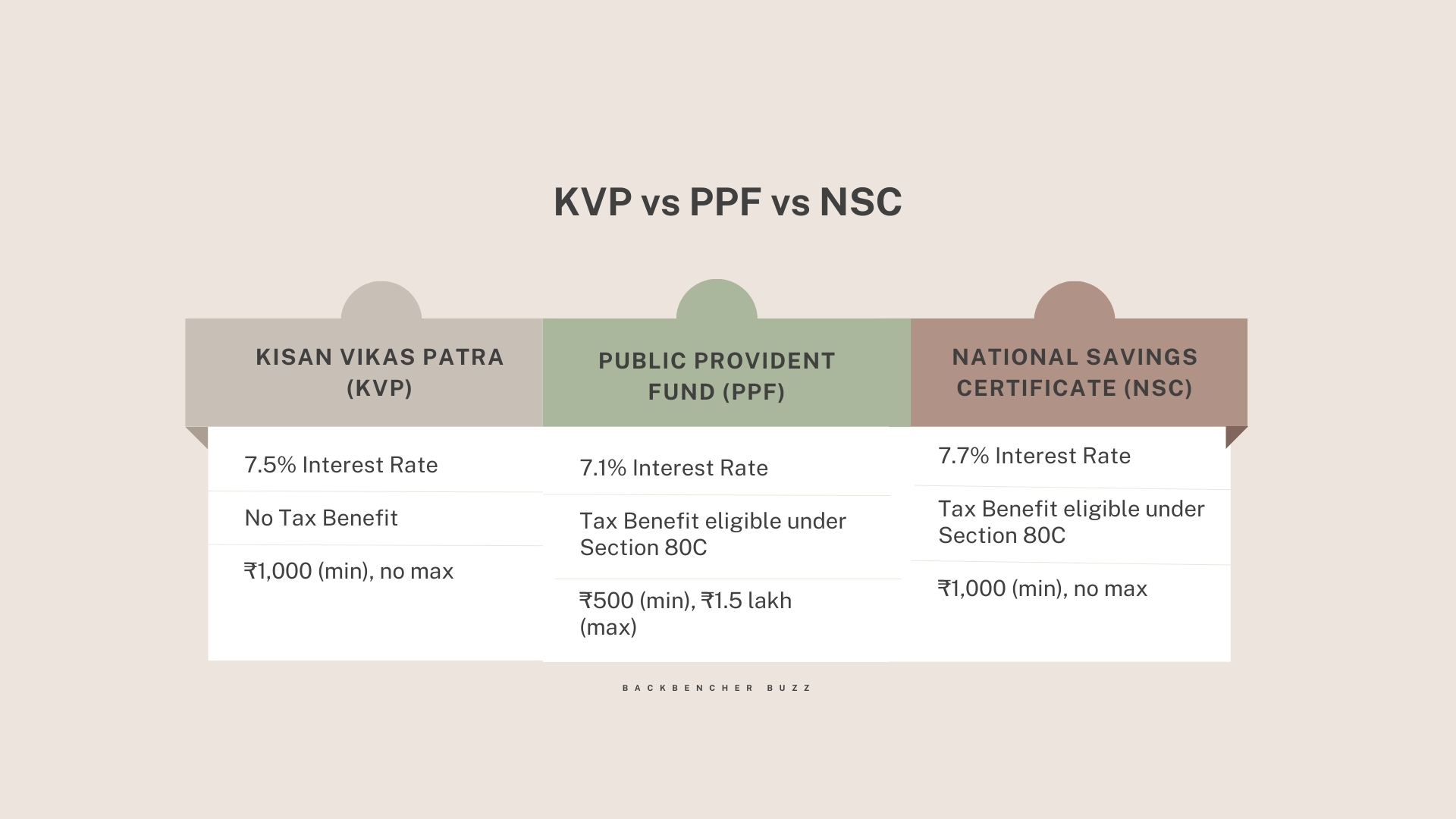

7.5% (Revised Quarterly)

Investment Doubling Time

115 months (9 years and 5 months)

Minimum Investment

₹1,000/-

Maximum Investment

No Limit

Lock-in Period

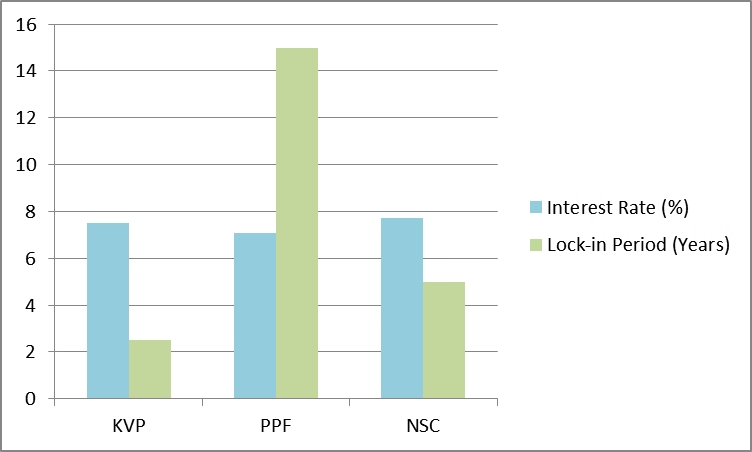

2.5 Years

Tax Benefits

No tax deduction under Section 80C; returns are taxable

Eligibility

Indian residents aged 18 years or older

Transferability

Can be transferred to another person or inherited

Premature Withdrawal

Allowed after 2.5 years or in exceptional cases like death of the holder

Calculate your KVP returns using our calculator

What Is Kisan Vikas Patra (KVP)?

The Kisan Vikas Patra is a fixed-income, government-backed savings bond that they open in post offices or banks across the country. This particular scheme caters to a low-risk profile investor who preferred safer means of doubling their savings at a guaranteed rate by the government of India. KVP was first launched in 1988, considering the changes in the financial landscape and the evolving needs of investors.

Key Features of Kisan Vikas Patra

Assured Returns: Fixed and secure returns offered by the KVP which are beneficial for risk free investors.

Investment Doubling: Kisan Vikas Patra has earned a respectable name for doubling investor money. The interest rate, which the government of India revises quarterly, most likely governs the time period for money to double.

Minimum and Maximum Investment: The KVP allows the smallest investment of ₹1,000/-, and the largest investment is uncapped. Hence, it is ideal for all investors.

Taxation: Kisan Vikas Patra does not offer tax benefits under Section 80C, but the returns are fully taxable. However, the maturity amount is exempt from TDS (tax deducted at source).

Transferability: KVP certificates are transferable between individuals. The investors are free to name beneficiaries, allowing seamless transfer in case of untoward disasters.

Premature withdrawal: An early withdrawal might take place due to the death of the holder or after two-and-a-half years of deposit.

Current interest rate for Kisan Vikas Patra

The latest updates say that Kisan Vikas Patra gives a yearly interest rate supposing the highest amount possible of 7.5% and doubling money at 115 months, that is, 9 years and 5 months. Besides, before making any investments, each investor must check the current rates since they change every quarter.

The eligibility criteria for Kisan Vikas Patra (KVP) are as follows:

Residence Status:

Indian Residents Only: KVP is issued only to Indian residents. As it is often with other Indian schemes, non-resident Indians cannot invest in this scheme.

Age:

Minimum Age: Minimum age prescribed is 18 years for the investor.

Minor Investors: A minor can also invest in KVP, but it has to made through a guardian which may include the parent or legal guardian of the minor.

Account Types:

Single Account: One or more persons may make deposits to KVP accounts under his or her name.

Joint Account: KVP can also be opened under nominees, that is, two or more people invest in the KVP.

Hindu Undivided Family (HUF): Hindu Undivided Family are not eligible to open KVP.

Investment by a Minor: If the investor is a minor, the investment has to be made in their name and a guardian has to manage the account.

Transferability: KVP certificates are assignable in that the holder can sell the certificates to another person, even before the certificates’ maturity, under certain circumstances.

No Upper Investment Limit: Today there is no maximum limit of investment KVP. The minimum amount of investment has to be ₹1000/-, and you can invest above this amount only. But for the certificate it is available in ₹1,000/-, ₹5,000/-, ₹10,000/-, ₹50,000/-.

Nomination Facility: It is also good to note that with the KVP you can name someone that will benefit from the KVP in the event that you die.

Benefits of Kisan Vikas Patra Investment

Low risk: Kisan Vikas Patra is a government-backed scheme that offers the option of risk-free investing with guaranteed returns.

Easy accessibility: KVP is accessible at all post offices or banks, allowing both rural and city inhabitants convenient access.

Flexible Investment Option: The KVP subscription is open to all amounts or values, without any upper limit. Hence, it draws investors ranging from small to large.

Financial Discipline: It encourages financial discipline termed forced lock-in period of 2.5 years, early long-term investment, or savings that motivate consumers to simplify the process of saving continuously.

Liquidity facilities: KVP is, however, not meant for access to short-term settlements, though partial liquidity availing may be exercised after the lapse of a minimum of 2.5 years.

How to Open KVP Offline

Step 1: Visit the Nearest Post Office or Bank

Visit your nearest post office or authorized bank branch that offers KVP.

Step 2: Fill Out the Application Form

Obtain the KVP application form and fill in details like:

Name

Address

Nominee details

Investment amount

Step 3: Submit Required Documents

Attach photocopies of the following:

Identity proof (Aadhaar Card, PAN Card, Voter ID, etc.)

The tax deduction benefits available under Section 80C are not provided by KVP unlike PPF and NSC which are other government saving schemes. Potential investors seeking tax benefits will not find KVP suitable because it does not provide any tax-saving advantages.

2. Long Maturity Period

The KVP investment requires 9 years and 5 months to double the initial amount when the current interest rate stands at 7.5%. The lengthy duration before KVP funds mature does not fulfill investors who seek both rapid returns and quick investment opportunities.

3.Limited Liquidity

The option to withdraw from KVP exists after 2.5 years but this scheme does not suit investors who need immediate access to their funds. The investment demands participants to extend their savings periods while accepting financial limitations on their deposited funds.

4.Interest Rate Variability

The government performs quarterly reviews to modify the interest rate thus affecting the investment returns. Your investment requires an extended time to double its value compared to traditional fixed-rate products because market conditions become less predictable.

5.Investment Lock-in for Minors

Minors can obtain KVP through their guardians when they buy this investment product. KVP provides parents with a way to invest for their children yet maintains limited control over the funds until their child becomes an adult.

6. No Interest Payout

KVP does not generate interest payments during the investment term because all accumulated earnings get paid out when the contract matures. The investment method of KVP does not work well for investors who depend on their investments to generate regular cash flow.

Frequently Asked Questions (FAQs)

1. What is Kisan Vikas Patra (KVP)?

Kisan Vikas Patra (KVP) is a government backed savings scheme for people to invest, earn guaranteed returns. This is a fixed income investment product with fixed rate which depends on the current interest rate and the amount involve doubles after a specific period.

2. Who can invest in KVP?

Investment in KVP is possible only by Indian citizens residing in India. The minimum investment of KVP is 18 years. Investing for minors is possible through a guardian.

3. What is the lowest and highest investment limit in KVP?

Minimum Investment is ₹1,000/-. In KVP too there is no upper limit of Maximum investment.

4. What is the rate of interest of KVP?

KVP interest rate currently (with respect to revision by the government every quarter) is 7.5% annually. This means, roughly, 9 years and 5 months to double your money.

The returns from KVP are taxed according to your income tax slab. KVP does not give tax benefits under Section 80C. But the maturity amount is not subjected to Tax Deducted at Source (TDS).

6. Can my KVP be transferred to someone else?

KVP certificates are transferable to other individuals. You can shift the ownership of your KVP certificate to any other person of your family or any other person, as per the terms of India Post or issuer of KVP.

7. What is the KVP maturity period?

The maturity depends on the interest rate. At the current rate of 7.5%, the investment will double in about 9 years and 5 months. The time to maturity changes with every change in interest rate i.e. every quarter.

8. To withdraw your KVP investment, can I withdraw?

Premature withdrawal is allowed after 2.5 years (death of the holder or with special permission) under KVP. Maturity: The accrued interest amounts will be added to the investment when it reaches maturity, amounting to a total amount you can withdraw from the post office or bank that has the investment.

9. Is KVP a safe investment?

Yes, KVP is a low risk and safe investment option, why, because KVP is backed by the government of India. Guaranteed returns, protected principal — that’s the deal.

10. Can KVP act as collateral for loans?

The KVP certificate can be pledged by you with financial institutions or banks as collateral to obtain a loan.

Conclusion

Kisan Vikas Patra (KVP) provides a secure savings growth opportunity that receives backing from the Government of India. The investment option of Kisan Vikas Patra provides guaranteed returns through its simple structure and easy accessibility to all investors seeking low-risk opportunities. Cheque that your investment matches your financial targets and your requirement for cash availability before you make a commitment.

Why let your money sit idle when it can grow? Invest in KVP today and in 9 years and 5 months it will double without any market risks. Just visit your nearest post office or bank and take the first step toward a secure financial future. Your future self will thank you!

Skip to content

Skip to content