Do you seek a risk-secure investment that provides better returns than what Fixed Deposits currently offer? Several investors aim to find investment opportunities which provide risk-free returns while offering tax advantages. One such trusted choice is the National Savings Certificate (NSC), which is a government backed scheme that offers 7.7% NSC interest rate with guaranteed returns.

The wide availability of NSC investment at Indian post offices makes this product suitable for new investors and tax planning purposes while providing long-term savings security. In this article, we will explore NSC benefits, comparison with other savings schemes and a step-by-step guide to investing helping you decide if NSC tax benefits aligns with your financial goals.

National Savings Certificate (NSC): Key Details at a Glance

Feature

Details

Interest Rate

7.7% (as of January 2025)

Investment Tenure

5 Years

Minimum Investment

₹100/-

Maximum Investment

No Limit

Tax Benefits

Section 80C of the Income Tax Act

Risk Level

Low (Government-backed scheme)

Maturity Amount (for ₹1,00,000)

₹1,38,500 after 5 years

Eligibility

Indian Residents Only

Premature Withdrawal

Allowed only in exceptional cases

Calculate your NSC returns using our calculator

What is National Savings Certificate (NSC)?

National Savings Certificate (NSC) is a low-risk investment government sponsored savings scheme which pays fixed, risk-free returns. The interest rate is 7.7% and it encourages long term investment and tax benefits under Section 80C of the Income Tax Act.

Key Features of National Savings Certificate

The features of the National Savings Certificate (NSC) help investors decide whether it matches their financial targets.

Trusted & Backed by Government:Backed by the Government of India, ensuring better security for investors.

Tenure: Fixed tenure is for 5 years which can be termed as medium-term investment.

Interest Rate:NSC interest rate is currently 7.7%, which is better than many Fixed Deposits.

Tax Benefits: Eligible for claim deductions up to ₹1.5 lakh under section 80C of the Income Tax Act.

Transferable: It may be transferred by an individual to another individual through assignment.

You can appoint a nominee to receive the maturity amount in case of your unfortunate demise.

NSC IX DISCONTINUED – NSC VIII IS OPERATIVE

NSC IX has been discontinued, and only NSC VIII remains active. The government withdrew NSC IX to simplify investment options and streamline the scheme. The modification was meant to facilitate the choice of investments there on and therefore hasten the undertaking procedures.

Investors can, however, hold unto the NSC IX certificates until maturity and earn interest according to the original terms. Currently, new investments can only be made under NSC VIII, which has a 5-year maturity period and offers NSC tax benefits under Section 80C. In this context, the NSC VIII offers attractive returns.

Benefits of Investing in National Savings Certificate

Risk-averse investors prefer National Savings Certificate investment due to features of NSC are attractive. Some of its benefits are:

Guaranteed Returns: Provide the guarantee of returns unlike market-linked instruments.

Tax Efficiency: Offers benefit up to ₹1.5 lakh as deductions (under Section 80C of the IT Act).

Compound Interest: The NSC interest calculation methods ensures that accumulated interest each year gets reinvested which results in increasing returns during subsequent annual periods.

Accessibility: These are easily available in rural and urban region making it convenient low-risk investment in post office.

Flexible Investment Amount: You can invest a minimum of ₹100/- and no maximum limit this is to ensure that it is for all income groups.

Eligibility Criteria for National Savings Certificate (NSC)

There are some eligibility criteria, keep in mind before investing in National Savings Certificate (NSC):

Indian Residency:

NSC is only for Indian residents to invest in.

NSC investments are not available to Non-Resident Indians (NRIs).

Age Limit:

No age limit exists for investment.

NSC may also be invested by a minor through his or her guardian.

Type of Ownership:

Individual, joint, or on behalf of a minor, NSC can be purchased.

Joint Accounts can be opened in two modes:

Joint A: Both are equal owners.

Joint B: The primary owner and the secondary owner are two holders.

Nomination:

The maturity proceeds in case of the death of the account holder can be received by any beneficiary of investors at the time of purchase or after purchase.

Transferability:

NSC certificates are transferable only once to another during the tenure.

Eligible individuals (e.g., gifting or inheritance) are permitted to one another transfers.

Investment Source:

Income earned from India is to be made an investment.

Investments must be made using income earned in India; funds from foreign sources are not allowed.

How to Invest in National Savings Certificate (NSC) Offline

To invest in NSC offline, follow the listed steps:

Step 1: Fetch the NSC application form online/post office.

Step 2: Fill all the details.

Step 3: In case of self attested copies required KYC documents, you need to submit the form.

Step 4: You pay an amount you have decided upon to invest and take the original documents for verification.

Step 5: If approved, use the NSC that you fulfil your application with.

How to Invest in National Savings Certificate (NSC) Online

Investing in NSC Online (If you have Net Banking access for your Post OfficeSavings Account) is straightforward. Follow these steps:

Step 1: Log in to Open Department of Posts (DOP) net banking.

Step 2: Click on Service Requests under ‘General Services’.

Step 3: Click on the New Requests and select NSC Account – Open an NSC Account (For NSC).

Step 4: Input deposit amount in and pick debit account towards PO savings account.

Step 5: Run through the terms and conditions and choose ‘Click Here’. Accept them once done.

Step 6: Type the transaction password and click on ‘Submit’.

Step 7: When the deposit receipt will be there to view and download.

Step 8: To see details for your National Savings Certificate (NSC) account, login, and click on ‘Accounts’.

Request for Duplicate National Savings Certificate

If you lost, left behind, stolen, destroyed, mutilated or changed (availed), you can demand for a duplicate NSC certificate. All you need to do is fill out the Duplicate Savings Certificates form handed to the post office where you wish to have the NSC replaced.

The following are the form’s key fields:

Other information, such as serial numbers, denominations, NSC issue and so on concerning the certificate(s).

The date the certificates were purchased on.

It should indicate the reason why a duplicate certificate should be filed also with additional details.

How NSC Interest is Calculated

Interest on National Savings Certificate (NSC) is compounded annually but paid upon maturity.

For example: If you had invested ₹1,00,000/- for 1 year at a rate of return of 7%, your money would stand at ₹1,07,000/- at the end of one year.

Present Interest rate is 7.7%, it will change for every six months.

The interest for next year is calculated on ₹1,07,000/- and so on.

Annual compounding significantly boosts the maturity amount after 5 years.

You can google search for National Savings Certificate (NSC) Calculator for calculating amount.

The National Savings Certificate has been backed by the government for one other reason-it offers tax benefits. However, it does come with its own forms of taxation, of which the following must be mindful:

Principal Amount: This allows a tax deduction under section 80C.

Interest Portion: This shall be taxable, but availing of further deductions under section 80C if reinvested is of benefit.

Maturity Amount: This includes principal and accrued interest which shall be taxed after adjusting for deductions availed during the term.

NSC vs Other Savings Schemes

Here’s a comparison:

Feature

NSC

PPF

Fixed Deposit

Tenure

5 Years

15 Years

Flexible

Interest Rate

Fixed by Govt

Fixed by Govt

Varies by Bank

Tax Benefits

Sec 80C

Sec 80C

Sec 80C (limited)

Risk Level

Low

Low

Low to Medium

Is NSC Right for You?

NSC is ideal for:

First-Time Investors: Simplified and government-backed, it’s perfect for beginners.

Taxpayers: Best for maximizing deductions under Section 80C.

Conservative Investors: Prioritizes capital safety over high returns.

Feature

NSC (National Savings Certificate)

FD (Fixed Deposit)

Interest Rate

7.7% p.a. (Annual compounding)

6.5% p.a. (Varies by bank)

Investment Tenure

5 years

5 years

Minimum Investment Amount

₹100

₹1,000

Tax Benefits

Tax deduction under Section 80C

Tax deduction under Section 80C

Interest Payout

Interest compounded annually, paid at maturity

Paid quarterly, half-yearly, or annually

Interest Calculation Method

Annual compounding

Simple or compound interest (depends on FD type)

Loan Against Investment

Loan facility available

Loan facility available

Liquidity

Locked for 5 years

Can be broken prematurely (with penalty)

Taxation on Interest

Taxable upon maturity (except principal)

Taxable upon maturity

Tax on Maturity Amount

Taxable

Taxable

Nomination Facility

Available

Available

Transferability

Transferable (can be assigned to others)

Not transferable

Maturity Amount (₹) (For ₹1,00,000 invested)

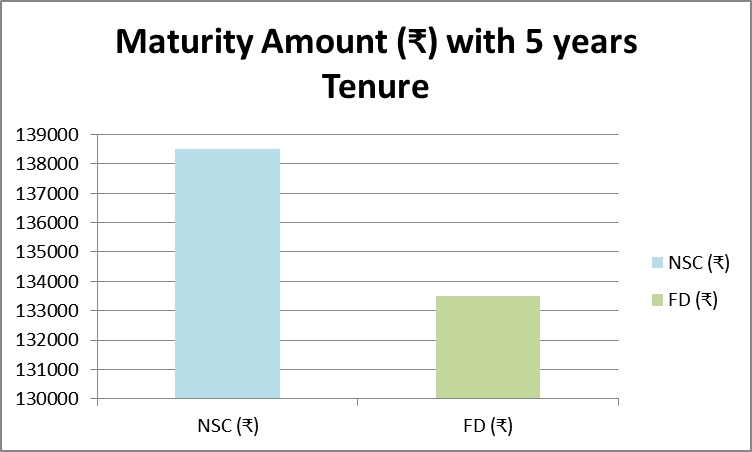

₹1,38,500 (after 5 years)

₹1,33,488 (assuming 6.5% interest)

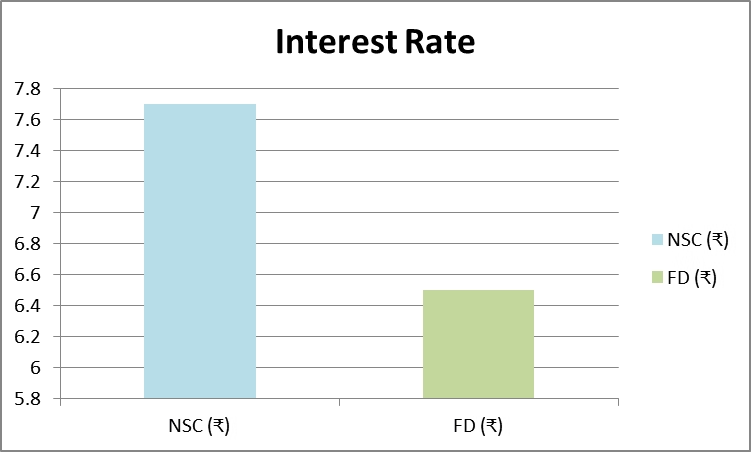

NSC vs FD – Which is Better? This bar graph compares the interest rates, tax benefits, and maturity returns of National Savings Certificate (NSC) at 7.7% and Fixed Deposits (FDs) at 6-7% in 2025. See which investment offers higher returns and tax savings!

Interest Rate: NSC provides a 7.7% fixed interest rate that exceeds the standard 6.5% rate available through Fixed Deposits thus making it an advantageous option for investors seeking stable returns.

National Savings Certificate NSC vs FD: Which gives better maturity returns? This bar graph shows how NSC’s 7.7% fixed interest rate beats FD’s 6.5% rate, resulting in a higher maturity amount after 5 years.

Maturity Amount: NSC offers a higher maturity amount after 5 years as the interest rate is better.

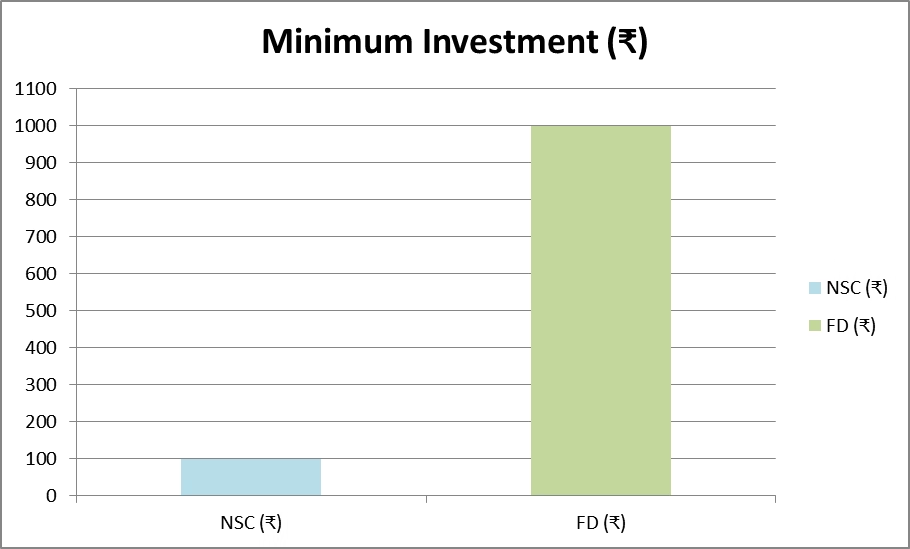

National Savings Certificate NSC vs FD: Minimum Investment Comparison – National Savings Certificate (NSC) starts at ₹100, while Fixed Deposits (FD) require a minimum of ₹1,000. See the difference in this bar graph!

Minimum Investment: According to the National Savings Certificate, an investment of ₹100/- is a minimum amount and hence lower than FD that needs ₹1,000/-.

Real Life Examples

Ravi, a 35-year-old salaried employee, wished to invest in a safe investment to save taxes and grow his wealth. Investing ₹1.5 lakh in NSC not only provided him with a tax deduction under Section 80C, but also compounded to ₹2,07,750 after 5 years, ensuring a safe financial future.

Anjali, a homemaker who wished to save her cash for a future emergency. She invested ₹50,000 in NSC at a 7.7% interest rate. After 5 years her investment had grown to ₹69,250 and she was able to build a safety net for her family.

Raj was considering a Fixed Deposit offering 6.5% interest, but after comparing, he realized NSC’s 7.7% interest rate would give him an additional ₹5,000 in maturity amount over 5 years. He chose NSC for better returns and tax benefits.

FAQs About National Savings Certificates (NSC)

1. Can I break NSC before maturity?

Premature withdrawals are permitted only in certain circumstances, such as the investor’s death or a court order.

2. I lost my NSC certificate — what can I do?

For a duplicate certificate, apply with required documents at the issuing post office.

3. Can I transfer my NSC?

Yes, NSC is transferable once during its tenure.

4. Is the interest earned on NSC taxable?

Yes, the interest earned is taxable. However, for the first four years, it is automatically reinvested and qualifies for a tax deduction under Section 80C. The final year’s interest is taxable.

5. Can NRIs invest in NSC?

No, only Indian residents can invest in NSC. NRIs are not eligible to purchase new NSC certificates.

6. Is NSC better than Fixed Deposits (FDs)?

NSC offers a higher interest rate (7.7%) than most bank FDs and provides tax benefits under Section 80C. However, FDs offer more liquidity since they allow premature withdrawals (with penalties).

7. Can I take a loan against NSC?

Yes, NSC can be used as collateral for a loan from banks and financial institutions. The certificate needs to be pledged to avail the loan.

If purchased online via Post Office Net Banking, you can track it under the “Accounts” section. For offline purchases, you need to keep the physical certificate or update your passbook at the post office.

9. What happens if I don’t withdraw NSC after maturity?

If you don’t withdraw your NSC after maturity, it will stop earning interest. However, you can claim the maturity amount anytime, as there is no maximum holding period after maturity.

10. Can I invest in NSC multiple times?

Yes, Of course, there is no limit to the number of NSC certificates you can buy. You can invest multiple times as long as you stay within the ₹1.5 lakh limit for tax benefits under Section 80C.

Final Thoughts: Should You Invest in NSC?

Looking for a safe, easy investment with guaranteed returns and tax benefits? The National Savings Certificate (NSC) could be just what you need! It is a good option for risk averse investors with 7.7 percent interest rate, full government backing and tax savings under Section 80C.

NSC is ideal for:

Those new investors who wish to have a simple and secure means of growing their savings.

Taxpayers who want to gain maximum deduction under Section 80C.

Those who prefer stability to market risks and are conservative investors.

However, diversification of your savings is always good. NSC is a good option, but you can also go for PPF, SCSS or Fixed Deposits to balance your investments.

Ready to invest? Just visit your nearest post office or apply online via the Department of Posts Net Banking portal today – it only takes a few minutes!

Skip to content

Skip to content

vs Fixed Deposit (FD) – Best Investment for 2025?")