For a long time, the National Pension System (NPS) has been at the heart of retirement planning in India. The Government of India introduced the NPS Vatsalya scheme a pension initiative for minorsin the Union Budget as a progressive measure to promote financial discipline from an early age. It is a child pension plan in India. Designed with minors, it aims to instill early retirement savings habits and ensure long-term financial security for minors (future generations).

Feature

Details

Target Group

All Indian minors (up to 18 years)

Eligibility

Parents/guardians can open the account on behalf of the minor

Minimum Contribution

₹1,000 per year

Maximum Contribution

No upper limit on contributions

Investment Options

Moderate (LC-50), Aggressive (LC-75), Conservative (LC-25), Active Choice

Account Transition at 18

The account automatically transitions to a regular NPS Tier I account

Tax Benefits

Contributions are not tax-exempt, but 60% of the corpus can be withdrawn tax-free

Corpus Growth Potential

Returns depend on market performance, offering ~10% potential returns

Partial Withdrawals

Allowed after 3 years (up to 25% for education, medical emergencies, disability)

Exit Options at Maturity

If corpus ≥ ₹2.5 lakh: 80% annuity, 20% lump sum withdrawal; if corpus < ₹2.5 lakh: Full withdrawal

KYC Process

KYC must be completed within 3 months of the child turning 18

Taxation on Withdrawal

40% of corpus must be used for annuity (taxable as per income tax slab)

How to Open Account

Through registered PoPs (banks, India Post) or eNPS platform

Partial Withdrawal Conditions

After 3 years, for education, medical emergencies, or disability

The NPS Vatsalya Scheme is a child pension plan in India regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It is designed for all Indian citizens below 18 years of age. The main purpose is to encourage the habit of saving for old age from an early age as well as to create a pensioned society.

How Does the NPS Vatsalya Scheme Work?

Think of it as a retirement savings plan for children! These funds are invested in different asset classes and parents or guardians can contribute to their child’s account. By the time the child turns 18, the retirement fund matures and is automatically converted into a regular NPS Tier I account. NPS (National Pension Scheme) is also similar but it is for adults.

Key Features of the NPS Vatsalya Scheme

Eligibility & Account Operation

Eligible for all minor citizens up to 18 years.

For minors, Parents/guardians can open the account on behalf of minors.

However, the minor is the sole beneficiary of the account.

Contribution Details

Minimum Contribution:₹1,000 per annum.

Maximum Contribution: It is flexible to deposit amounts with no maximum limit.

Investment Choices

Default Choice: Moderate Life Cycle Fund (LC-50) with exposure to 50% equity defaults.

Auto Choice: Aggressive (LC-75), Moderate (LC-50), or Conservative (LC-25) funds are available as Auto Choice.

Active Choice: Guardians can actively choose the allocation among equity, corporate debt, government.

Transition at Maturity

While the child turns 18, the NPS Vatsalya Scheme account transitions into a regular NPS Tier I account.

A fresh Know Your Customer (KYC) process must be completed within 3 months of turning 18 to continue contributions.

Flexibility in Contributions: Parents contribute based on their financial capability.

Investment Growth Potential: The compounded growth offers options of equity, corporate debt and government securities.

Real- Life Examples: How Parents Are Using NPS Vatsalya

1. Middle class parent makes smart investment.

Amit & Priya, a couple from Pune, wanted to secure their daughter’s retirement from an early age. They decided to contribute ₹10,000 per year starting when she was 5 years old.

By the time their daughter turns 18, their investment of ₹1.3 lakh grows to ₹3.5 lakh (assuming 10% returns). They didn’t withdraw it; it stayed in NPSand provided their daughter a huge head start in retirement planning.

Lesson: Compounding! Tiny contributions can add up overtime.

2. Grandparents Securing Their Grandchild’s Future

Mr. Sharma (68) wanted to give his grandson a financial gift that lasts a lifetime. Instead of a fixed deposit, he opened an NPS Vatsalya account and deposited ₹50,000 annually.

By the time the grandson turns 18, the corpus grows to ₹20 lakh. This amount later transitions into a full-fledged pension scheme, ensuring a financially independent future.

Lesson: One time investment can lead to one life time benefits!

Contributions to NPS Vatsalya: Currently, contributions to the scheme are not tax-exempt under Section 80C.

Tax on Withdrawal:

Upon attaining 18 years:

60% of the corpus can be withdrawn tax-free.

40% must be used to purchase an annuity, which is taxable as per the individual’s income tax slab.

If the corpus is less than ₹2.5 lakh: The entire amount can be withdrawn tax-free.

Annuity Taxation: The pension received from the annuity will be taxed as per the individual’s applicable tax slab.

Contribution vs. Growth Table

This table shows how different yearly contributions impact the corpus by the time the child turns 18.

Yearly Contribution

Total Invested (18 Years)

Corpus at 18 (10% Returns)

₹5,000

₹70,000

₹1.75 Lakh

₹10,000

₹1.3 Lakh

₹3.5 Lakh

₹20,000

₹2.6 Lakh

₹8 Lakh

₹50,000

₹6.5 Lakh

₹20 Lakh

Higher contributions & early investments = Bigger corpus at maturity!

For creating long term wealth, high growth is preferred and then NPS Vatsalya is better than SSY and PPF as they have equity exposure and flexibility.

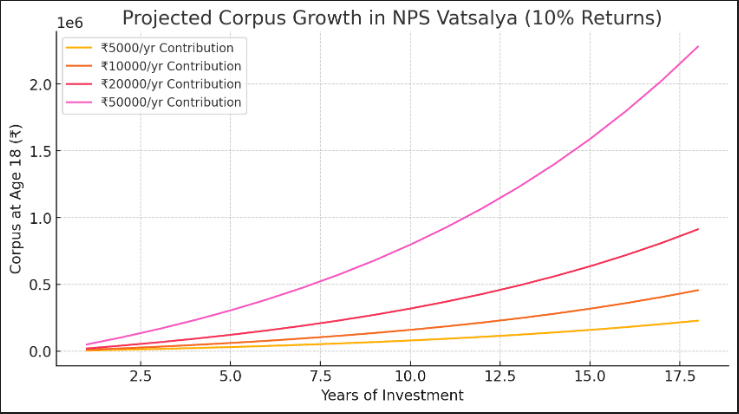

Projected Corpus Growth Chart

Visual presentation can motivate savings based on how savings accumulated over time. In the following graph, I plot potential corpus growth based on different levels of contribution and returns on the market.

The example illustrates how a final amount when the child is 18 years old will be generated with different contribution levels. You will observe how early and continuous contributions result in exponential growth from compounding.

How to Open NPS Vatsalya Account

Step 1: Choose an Enrollment Method

Visit any registered PoP (major banks, India Post, Pension Funds).

Use the online eNPS platform provided by NPS Trust.

Step 2: Complete Registration

Provide minor’s and guardian’s details.

Choose a Central Recordkeeping Agency (CRA).

Step 3: Submit Required Documents

For the Minor: Birth Certificate, Passport, PAN or any other valid proof of date of birth.

For the Guardian: Aadhaar, PAN or Voter’s ID, among other such documents.

Step 4: Make Initial Contribution:

Minimum of ₹1,000 per annum.

Step 5: Receive PRAN

A Permanent Retirement Account Number (PRAN) will be issued for future transactions.

NPS Vatsalya Withdrawal & Exit Rules

Partial Withdrawals

Allowed after 3 years.

Up to 25 percent of all contributions (not returns) can be withdrawn as contributions to education, medical emergencies or disability.

Exit Options Upon Turning 18

If corpus ≥ ₹2.5 lakh:

80% must go into an annuity.

20% can be withdrawn as a lump sum.

If corpus < ₹2.5 lakh:

Full withdrawal allowed.

In the event of the minor’s demise

The entire accumulated corpus is paid to the guardian.

How Does NPS Vatsalya Compare with Other Child Investment Plans?

Many parents may wonder how NPS Vatsalya stacks up against other popular child savings schemes. Here’s a quick comparison:

NPS Vatsalya offers a significant advantage in long-term wealth creation over SSY and PPF due to its Equity exposure, while SSY and PPF provide only fixed returns. If your aim is for retirement too, then NPS Vatsalya is a better option.

FAQs about NPS Vatsalya

1. Who can open an NPS Vatsalya account?

Any Indian citizen below 18 years can have an NPS Vatsalya account, operated by a parent or legal guardian.

2. When the child becomes 18, what happens to the account?

The account transitions into a regular NPS Tier I account, requiring fresh KYC within three months.

3. Can I withdraw money before my child turns 18?

After three years, It is allowed to make partial withdrawals for education, medical emergencies, or severe disabilities.

4. How is NPS Vatsalya different from Sukanya Samriddhi Yojana (SSY) or PPF?

NPS Vatsalya has a market-linked return (~10% potential), while SSY and PPF offer fixed returns (7.1% respectively). Additionally, SSY is only for girls, whereas NPS Vatsalya is open to all minors.

5. Are there tax benefits for contributing to NPS Vatsalya?

While contributions are not exempt from taxes, the corpus will be subjected to tax once withdrawn; however, SSY and PPF are tax free corpus.

The NPS Vatsalya scheme is a forward-thinking initiative that ensures financial security from an early age. Not only does it teach children to save, it prepares them to enjoy a good and stable life during retirement. Unlike traditional savings schemes, its equity component offers higher return potential over long term.

If you want to start to secure your child’s financial future, then this is where you should begin. To open an NPS Vatsalya account today, log in to eNPS or go to your nearest PoP. Today’s small step will eventually lead to tomorrow being financially independent!

Skip to content

Skip to content